The Central Bank of Liberia’s 2024 Annual Report delivers a warning that we cannot ignore: the country’s commercial banking sector is in sustained and worsening decline. The numbers are not just discouraging, they reflect deep institutional vulnerabilities and policy inertia that now threaten the recovery agenda of the Boakai-Koung administration.

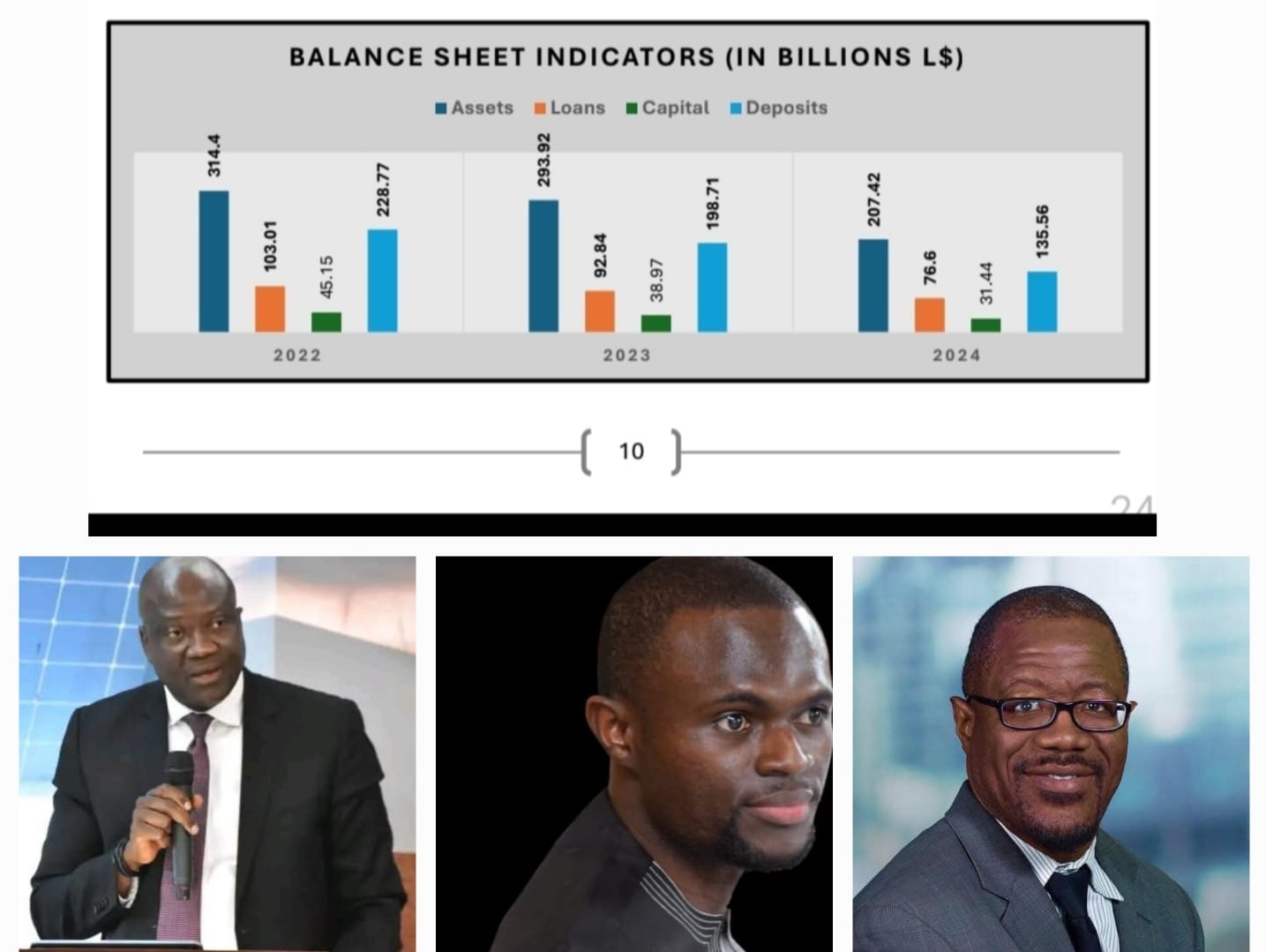

Between 2022 and 2024- four balance sheet indicators of a healthy banking sector- total assets, bank capital, deposit and credit to the economy—posted back-to-back annual declines. Commercial banks’ total assets, the value of what the banks own and can deploy to support the economy, contracted from L$314.4 billion in 2022 to L$207.42 billion in 2024—a staggering 34% drop. Over the same period, bank capital, the sector’s shock-absorbing buffer, fell from L$45.15 billion to L$31.44 billion, a 30% erosion in financial stability. Loans, which are vital for investment, growth, and job creation, dropped from L$103.01 billion to L$76.6 billion, a 26% contraction. At the same time, customer deposits, a core measure of public trust in the banking system, plunged by 41%, from L$228.77 billion to L$135.56 billion.

The data shows that the downturn started in 2022 and 2023 during Weah’s administration but that the contraction deepened during the first year (2024) of President Boakai’s administration. For example, the drop in total bank assets between 2023 and 2024 amounted to L$86.5 billion, more than four times the decline posted for 2022 and 2023. Deposits fell by L$63.15 billion under the Boakai administration—more than double the previous year’s loss. The decline in credit under the Boakai administration (L$16.24 billion) surpassed the L$10.17 billion drop in 2023. This is the hidden collapse we can no longer ignore!

The implications of the decline are profound. A shrinking banking sector undermines the government’s ability to mobilize domestic capital, and it cripples access to credit for small and medium-sized enterprises. They impede poverty reduction, job creation, and inclusive growth; the core promises of the ARREST Agenda for Inclusive Development (AAID). AAID places private sector expansion at the heart of its economic strategy, but that ambition is incompatible with reality in the banking sector. It is clearly impossible for the current trend in banking system to channel resources into the real economy to as needed, but despite these signals, there is no policy response of sufficient scale or urgency.

Early in 2024, the “RESCUE” administration took a positive step by commissioning an audit of the Central Bank. Conducted by the General Auditing Commission, the audit found widespread financial mismanagement and governance lapses and issued an adverse opinion—a rare and serious verdict in public sector financial auditing. The report cited “material weaknesses” affecting the Central Bank’s operations and called for urgent executive and legislative action.

This moment could have marked a turning point. But instead of using the audit as a launchpad for reform, the administration backed away from accountability. Governors of the bank implicated in mismanagement were rewarded with hundreds of thousands of U.S. dollars in exit benefits while mid-mangers that were used as agents of loots and corporate gangsterism remain with the bank, probably to execute another similar mission. Credible reports suggest that the reward decision was influenced by actors close to the presidency who traded personal financial gain for accountability; reinforcing the idea that many policy makers in Liberia are more tolerant of failure than committed to accountability and reform.

Fix the Banks or Fail the Nation: Urgent Fix The Banking System Needs That Liberia Can Not Ignore.

It is not late to reverse the course but doing so will require bold, coordinated action from both the Central Bank and the Ministry of Finance. Regulatory reforms must be enforced to ensure compliance with capital adequacy, risk controls, and governance standards. But even more urgently, public trust must be rebuilt, and confidence in the banking system restored.

A credible response must prioritize restoring the functionality and attractiveness of the banking system to the micro, small and medium sized (MSMEs) businesses in the real economy. This could include rolling out a credit stimulus facility to de-risk lending to MSMEs through strategic partnerships among the Central Bank, the Ministry of Finance, and commercial banks. At the same time, the government must invest in expanding digital banking infrastructure and modernizing transaction systems to make banking faster, more efficient, and responsive to the needs of small businesses—many of whom now avoid the banks due to delays and poor service delivery. To complement these efforts, a national banking literacy campaign should be launched, targeting entrepreneurs and informal sector actors through their organizations, to build trust, increase their banking footprints and enable them benefit additional banking services. The government must anchor these initiatives with safeguards that prevent elite capture and ensure benefits flow to productive enterprises and not used for political reasons.

Liberia cannot achieve inclusive growth while its banking system is declining. And because the decline is not a seasonal downturn, but a result of structural deterioration and institutional inaction, the Central Bank must return to its core mandate of safeguarding monetary and financial stability and the executive must lead with the courage to replace, penalize, and reform where necessary. The cost of continued inaction is already visible: falling investor confidence, reduced access to credit, rising unemployment, and deepening poverty. While the Boakai-Koung administration still has tools at its disposal—and the time to use them— the window is closing fast, and the lack of policy response of sufficient scale or urgency leaves much to desire.Ambulah Mamey is a Practitioner in International Development. He manages a portfolio of multi-sector USAID-funded resilience programs in Somalia, Tanzania, and Burundi. The opinions expressed here are his own and do not represent his employer.

Discussion about this post